Value Added Tax (VAT) for retailers in UAE was introduced on 1 January 2018 at a standard rate of 5% and is administered by the Federal Tax Authority (FTA).

Understanding VAT obligations is essential to avoid penalties, protect cash flow, and maintain full compliance with UAE VAT law.

VAT Registration Requirements for Retailers

- Mandatory registration when taxable supplies exceed AED 375,000

- Voluntary registration available when supplies exceed AED 187,500

- VAT registered businesses receive a Tax Registration Number (TRN)

- Retailers must charge 5% VAT on taxable sales

Key VAT Concepts for Retail Businesses

- Output VAT: VAT collected on retail sales

- Input VAT: VAT paid on purchases and imports

- Net VAT Payable: Output VAT minus recoverable Input VAT

- Zero-Rated Supplies: 0% VAT with input recovery allowed

- Exempt Supplies: No VAT charged and no input recovery

- Reverse Charge Mechanism (RCM): Self-accounting VAT on imports

VAT on Imports & Reverse Charge Mechanism (RCM)

Retailers importing goods into the UAE are subject to 5% VAT on the customs value. VAT-registered businesses account for this under the Reverse Charge Mechanism (RCM) within their VAT return.

Imported services such as foreign advertising, SaaS subscriptions, cloud services, and overseas consulting must also be reported under RCM.

From 1 January 2026, internal self-invoicing for RCM transactions is no longer required, but supporting documentation must be retained for audit purposes.

VAT Return Filing – VAT201 Form

Retailers must file VAT returns periodically through the FTA portal. Key VAT201 sections include:

- Box 1 – Standard rated retail sales (5%)

- Box 2 – Exempt supplies

- Box 3 – Reverse charge imports

- Box 4 – Zero-rated supplies

- Box 9 – Recoverable input VAT

- Box 10 – Net VAT payable or refundable

Accurate reconciliation with accounting records and customs documentation is essential.

VAT Record-Keeping Requirements

- Sales invoices and tax invoices

- Purchase invoices

- Customs import documentation

- Supplier invoices for imported services

- Accounting and bank records

Records must be maintained for at least five years under FTA regulations.

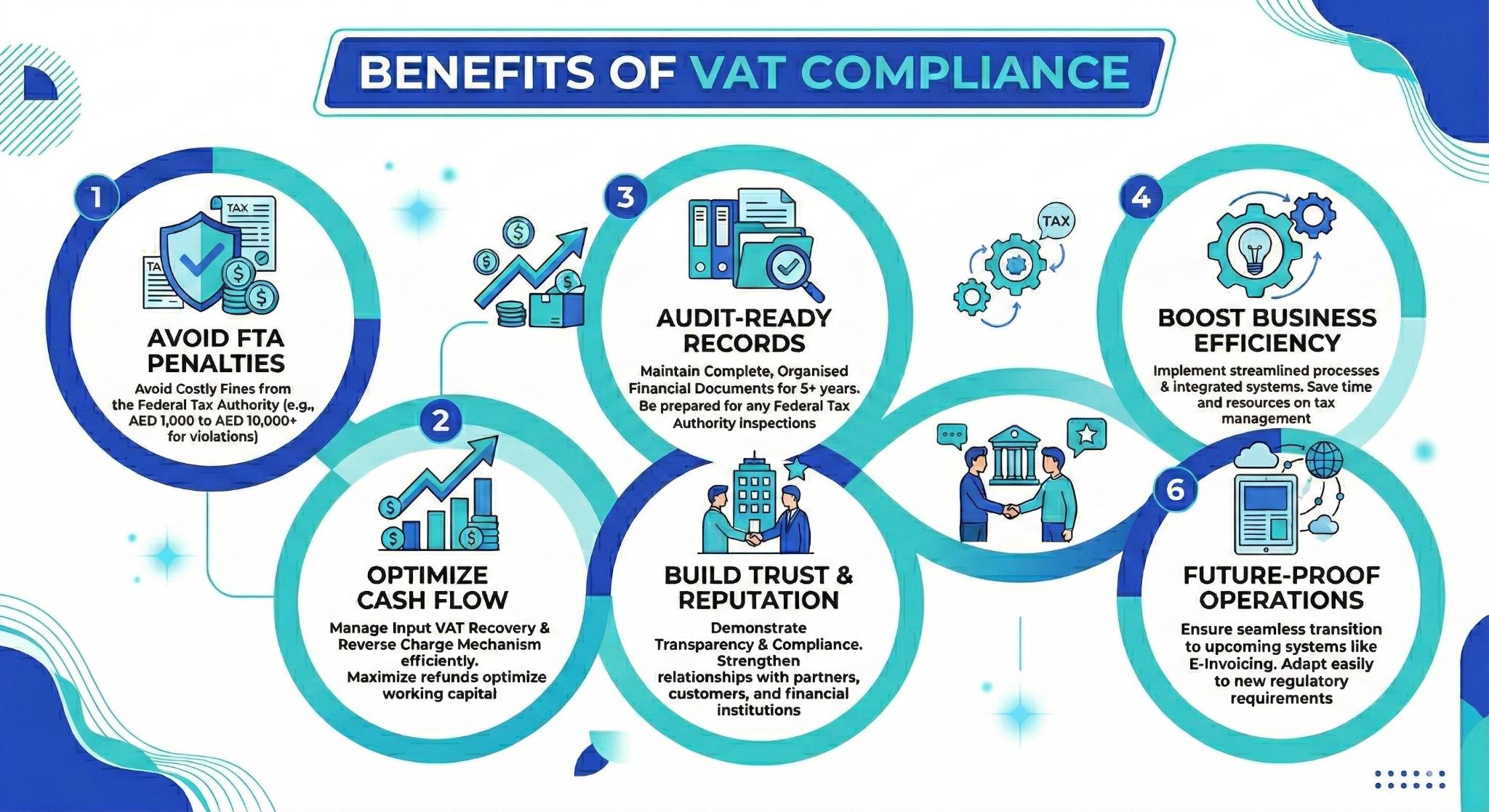

Key Benefits of VAT Compliance for Retailers in UAE

Strong VAT compliance helps retailers avoid Federal Tax Authority (FTA) penalties, protect input VAT recovery, maintain audit readiness, and ensure accurate reporting under UAE VAT regulations.

VAT Penalties for Retailers in UAE

- Failure to register: AED 10,000

- Late VAT return filing: AED 1,000 (first), AED 2,000 (repeat)

- Late payment penalties apply progressively

- Failure to issue tax invoices: AED 5,000 per document

- Failure to display VAT-inclusive prices: AED 15,000

Non-compliance may significantly impact profitability and business reputation.

Retail Industry VAT Implications

- Electronics & Mobile: 5% VAT; imports under RCM

- Clothing & Fashion: 5% VAT; discount treatment impacts VAT base

- Grocery & Food: 0% basic food, 5% processed items

- Jewellery & Gold: 5% retail jewellery; certain metals zero-rated

- Hardware & Building Materials: 5% VAT; installation services taxable

Correct product classification and import accounting are critical for compliance.

How Finsphere Supports Retail VAT Compliance

At Finsphere Global, we provide specialized VAT advisory services for retailers operating in the UAE.

- VAT registration and TRN setup

- Product VAT classification review

- Import & RCM advisory

- VAT201 return preparation and reconciliation

- E-invoicing implementation support

- FTA audit representation and penalty mitigation

We ensure your retail business remains compliant, audit-ready, and financially protected.

Frequently Asked Questions – VAT for Retailers in UAE

Do retailers in UAE need to register for VAT?

Retail businesses must register for VAT if taxable supplies exceed AED 375,000 in the past 12 months or are expected to exceed that amount within 30 days. Voluntary registration applies at AED 187,500.

What VAT rate applies to retail sales in UAE?

The standard VAT rate in the UAE is 5% on most retail goods and services. Certain basic food items and qualifying supplies may be zero-rated.

How does the Reverse Charge Mechanism (RCM) affect retailers?

Retailers importing goods or services must account for VAT under the Reverse Charge Mechanism (RCM). The VAT is declared in the VAT return as both output and input VAT, subject to recovery conditions.

What are common VAT penalties for retail businesses?

Common penalties include AED 10,000 for failure to register, AED 1,000 for late VAT return filing (AED 2,000 for repeat offenses), and additional penalties for late payment, missing invoices, or incorrect VAT reporting.

How long must retailers keep VAT records in UAE?

Retailers must retain VAT-related records, including invoices and customs documents, for at least five years under Federal Tax Authority (FTA) regulations.

Will e-invoicing be mandatory for retailers in UAE?

Yes. From 2026, VAT-registered retailers must issue structured electronic invoices and integrate their POS or ERP systems with FTA reporting infrastructure.

Strengthen Your VAT Compliance in UAE

Many businesses in the UAE remain focused on operations and growth but overlook the financial risks associated with improper VAT compliance. Without accurate VAT reporting, proper input tax recovery, and structured documentation, businesses may face penalties, cash flow disruptions, and audit exposure.

Our professional VAT advisory services in the UAE provide structured compliance, accurate VAT return preparation, and proactive regulatory support allowing you to focus on running your business while your VAT obligations are managed efficiently and in full alignment with Federal Tax Authority (FTA) regulations.

Contact Finsphere today to strengthen your VAT compliance framework and protect your business with expert tax advisory support.